Dear All,

The Hon’ble Finance Minister, Smt. Nirmala Sitharaman, presented the Union Budget 2025-26 on February 1, 2025, marking her eighth consecutive budget. The Finance Bill 2025 has received assent on March 29, 2025. The Finance Bill 2025 proposes several amendments aimed at simplifying tax compliance, encouraging voluntary compliance, and promoting investment and employment.

Below are the key direct tax amendments applicable from April 1, 2025:

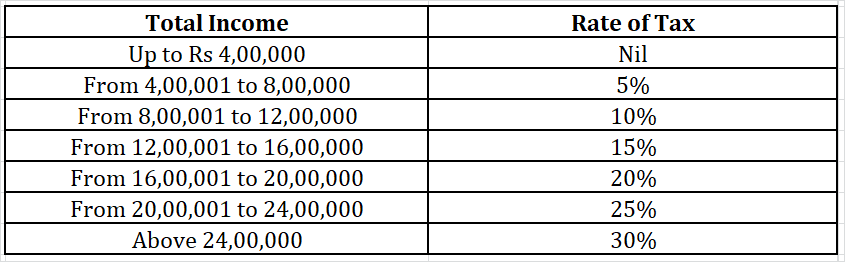

1. Change in Individual Income Tax slab rate (New tax regime) are as follows for FY 2025-26:

2. The total income limit for claiming this rebate increased to Rs. 12,00,000/- and accordingly, the rebate amount will be Rs. 60,000. It is applicable only for New Tax Regime.

3. The time limit for filing an updated return extended from 24 months to 48 months, with additional income tax payable structured as:

- 60% of the aggregate tax and interest for returns filed between 24-36 months.

- 70% of the aggregate tax and interest for returns filed between 36-48 months.

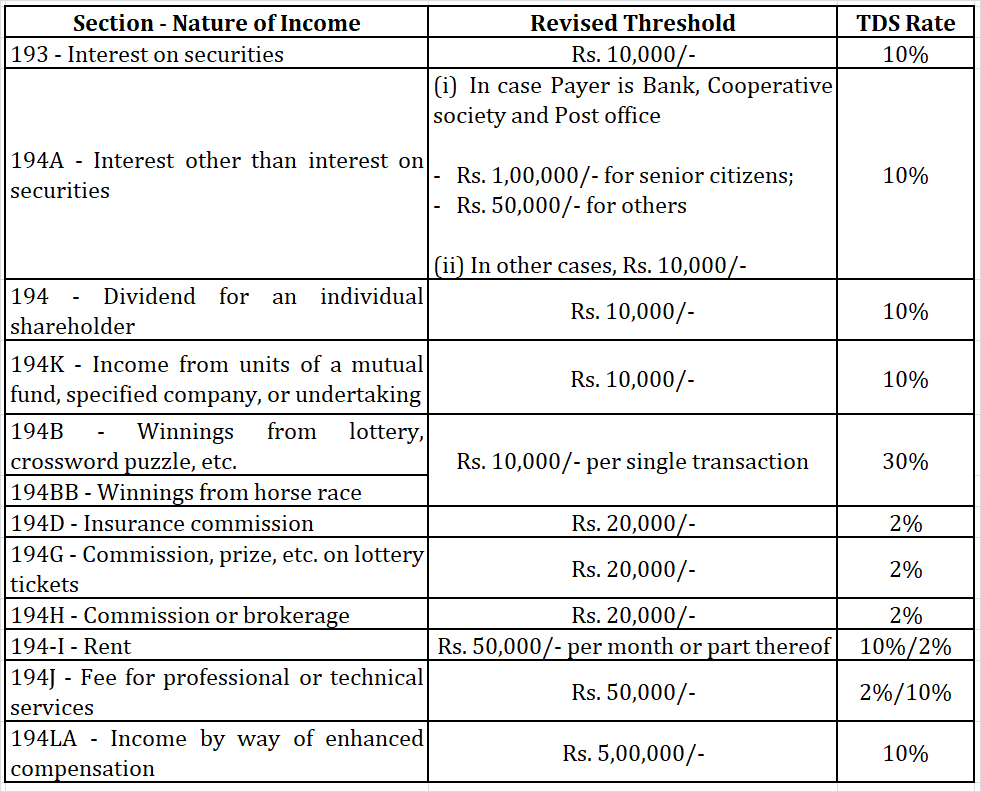

4. Enhancement of threshold for Tax deduction:

5. Under Section 194LBC, tax is required to TDS rate reduction for Section 194LBC be deducted at the rate of 25% (in case of individual or HUF) or 30% (other than individual or HUF) when a payment is made by a securitization trust to a resident investor in respect of their investment in the trust. As this trust is now sufficiently organized and regulated, the TDS rates under this section have been reduced substantially to 10 % in case of all the assessee.

6. Section 206C(1H) (TCS on Sale of specified goods) will not be applicable from April 1, 2025.

7. Sections 206AB and 206CCA (higher TDS/TCS for non-filers) have been removed from April 1, 2025.

8. Interest on delay in depositing TCS increased from 1% to 1.5% for every month or part thereof.

9. The equalisation levy on specified services will no longer apply from April 1, 2025. This change offers significant relief to non-residents from India’s “digital tax” framework.

Certain amendments introduced through the Finance (No. 2) Bill, 2024, which will come into effect from April 1, 2025 One such amendment mandates that any payments made by a partnership firm to its partners in the form of salary, remuneration, commission, bonus, or interest will be subject to TDS at a rate of 10% if the total amount paid during the financial year exceeds Rs. 20,000/-.

Furthermore, we have provided a detailed compilation of the key amendments proposed in the Finance Bill, 2025. To access the complete details, please click on the this link.