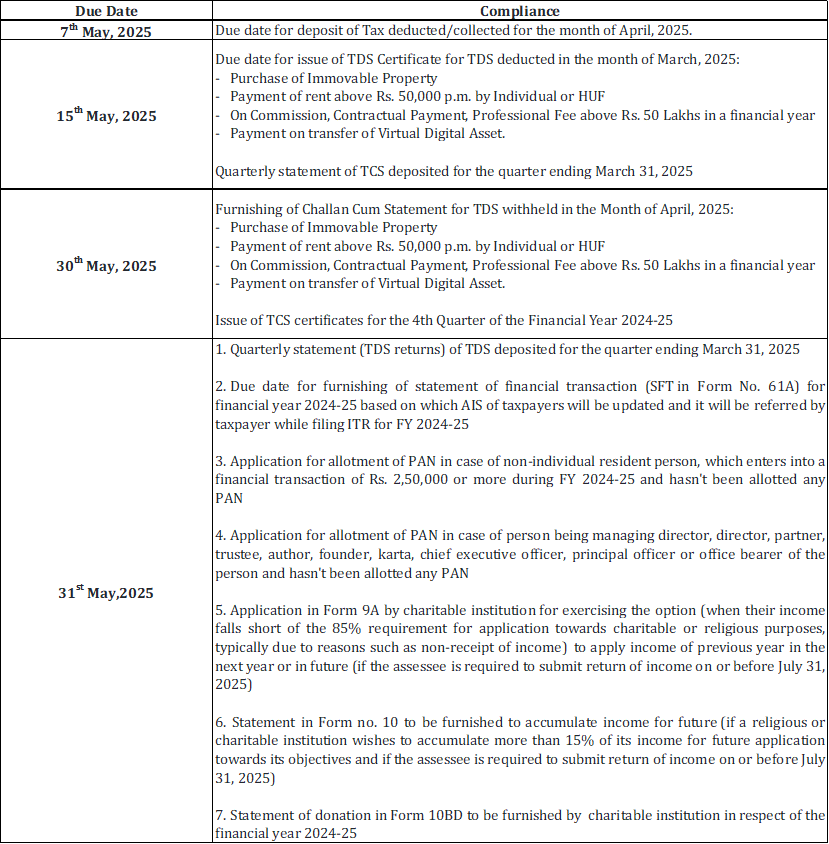

Due Date for Income tax Compliance – May 2025

Income Tax Updates – April 2025

1. Section 206C of the income-tax act, 1961 – collection of tax at source Notification S.O. 1825(E) [NO. 36/2025/F. NO. 370142/11/2025-TPL], DATED 22-04-2025

Income Tax provides for tax collection at source by certain persons at a specified percentage of tax from their buyers on specified transactions. TCS is already applicable on Motor car purchase wherein value is above 10 lacs.

Vide notification dated 22nd April, few more luxury goods (wristwatches, art pieces, collectibles, yachts, helicopters, sunglasses, handbags, shoes, sports gear, home theatre systems, and horses for racing or polo) are added in the said category wherein TCS will be applicable and buyer will be required to pay cost plus TCS of 1% on the same. However, buyers will be able to claim TCS in ITR.

Income Tax Judgements

2. Additions for bogus purchases, where the Tribunal and CIT(A) accepted purchases as genuine for most suppliers except two. The High Court upheld full disallowance only for those two due to lack of bank statement verification. | Principal Commissioner of Income-tax vs. Ganesh Developers [2025] 172 taxmann.com 542 (Bombay)[05-03-2025]

Facts of the Case:

Ganesh Developers, a firm engaged in the real estate business, filed its return of income for the Assessment Year 2010–11. The Assessing Officer (AO), during scrutiny proceedings, made a substantial addition of ₹14.30 crore under Section 69C of the Income-tax Act, alleging bogus purchases from various suppliers. An additional ₹50 lakh was added under Section 68. Although the assessee had initially failed to satisfactorily prove the purchases during assessment, it later submitted additional documents before the Commissioner of Income Tax (Appeals). In the remand proceedings, the AO independently verified bank statements of most suppliers and found no cash withdrawals after cheque deposits, thus substantiating the genuineness of those transactions. However, two suppliers—Neptune Trading Co. (NTC) and Hari Om Traders (HOT)—did not submit their bank statements, preventing further verification. The CIT(A) accepted the purchases as genuine in all cases except for NTC and HOT, for whom additions were retained at 12.5% of the purchase value. The Income Tax Appellate Tribunal upheld this order in full.

Issue Involved:

The central question before the High Court was whether the Tribunal erred in confirming only a partial disallowance (profit estimation) on purchases held to be unproven, instead of disallowing the entire amount under Section 69C. The Revenue argued that once purchases are found to be bogus or unverified, as in the case of NTC and HOT, the entire purchase amount should be disallowed, relying on the Gujarat High Court’s judgment in N.K. Industries Ltd., which had been upheld by the Supreme Court.

Tribunal’s Decision:

The Bombay High Court concurred with the CIT(A) and Tribunal’s findings in respect of all suppliers other than NTC and HOT, holding that the purchases were substantiated through detailed evidence and independent verification by the AO. Since there were no cash withdrawals from these suppliers’ bank accounts post cheque payments, the purchases were deemed genuine. However, for NTC and HOT, the Court found that in the absence of bank statements, the genuineness of transactions could not be verified. Moreover, since the assessee itself had accepted a 12.5% addition on these transactions and had not appealed further, it was held to have impliedly admitted that the purchases were not fully substantiated. The Court therefore ruled that the entire purchase amounts from these two suppliers should be disallowed and reversed the Tribunal’s order to that extent. Nevertheless, it limited the total disallowance to ₹1 crore, being the full value of purchases from NTC and HOT. Accordingly, the appeal was partly allowed in favour of the Revenue.

3. Whether unexplained credits in the bank accounts of an accommodation entry provider could be taxed in full under Section 68 when the assessee failed to identify the beneficiaries| Principal Commissioner of Income-tax vs. Buniyad Chemicals Ltd. [2025] 172 taxmann.com 462 (Bombay)[17-03-2025]

Facts of the Case:

Buniyad Chemicals Ltd., the assessee, was engaged in the business of providing accommodation entries. For Assessment Year 2009–10, the Assessing Officer (AO) made an addition of ₹10.73 crore under Section 68 of the Income-tax Act, 1961, treating credits in the assessee’s disclosed and undisclosed bank accounts as unexplained. During assessment, the director of the company admitted that they provided accommodation entries to clients for a commission of 0.15%, but failed to provide any information or documentation identifying the beneficiaries behind the credits. The AO concluded that these credits were unexplained and added them as income from other sources. The Commissioner of Income Tax (Appeals) [CIT(A)] held that if the assessee identified the beneficiaries, a commission rate of 0.37% should apply, but if not, the entire amount should be treated as unexplained income. The assessee appealed to the Tribunal, which instead restricted the addition uniformly to 0.15% of the total credits, without distinguishing between explained and unexplained entries.

Issue Involved:

The primary issue was whether the Tribunal erred in uniformly applying a 0.15% commission rate on all credits—both explained and unexplained—when the assessee had failed to furnish the required details of identity, source, and genuineness as mandated under Section 68. Another issue was whether the Tribunal’s reliance on its past orders, without analysing the facts and law afresh, was justified given the serious nature of the violations admitted by the assesse.

Tribunal’s Decision:

The Tribunal had directed that only 0.15% of the total deposits (regardless of whether the beneficiaries were identified or not) be treated as the assessee’s income, relying on its earlier decisions. However, the Bombay High Court found this approach to be legally flawed and factually casual. The Court held that unexplained credits cannot be treated as mere commission income, especially when the assessee failed to disclose beneficiary identities for over 3,300 transactions. The Tribunal was criticised for ignoring the mandatory requirements of Section 68 and for failing to consider the director’s statement made under oath, which clearly acknowledged involvement in fraudulent accommodation entries. The High Court restored the order of the CIT(A) with a modification: where beneficiaries are identified, commission income should be assessed at 0.15% (instead of 0.37%); for unidentified beneficiaries, the entire amount is to be treated as unexplained income under Section 68. The appeal was thus partly allowed in favour of the Revenue, reversing the Tribunal’s order.

4. Amendment introduced by Finance Act, 2020, increasing tolerance limit under section 56(2)(x)(b)(B) from 5 per cent to 10 per cent, has retrospective effect and applies to assessment year 2018-19. National Faceless Assessment Centre, Delhi vs. NRB Developers [2025] 172 taxmann.com 385 (Mumbai – Trib.)[25-02-2025]

Facts of the Case :

In the Assessment Year 2018–19, NRB Developers purchased a commercial property for ₹8.19 crore from M/s Lotus Griha Nirman Pvt. Ltd. The allotment letter was issued on 30 March 2010 after a booking payment of ₹3.5 crore through banking channels. However, at the time of property registration, there was a significant discrepancy of ₹9.04 crore between the stated purchase price and the stamp duty valuation. The Assessing Officer (AO), without providing the assessee with the DVO’s valuation report, treated the entire difference as income under Section 56(2)(x) of the Income-tax Act. On appeal, the Commissioner (Appeals) later obtained the DVO report, which valued the property based on the 2009–10 rate—corresponding with the allotment date—and limited the addition to ₹81.19 lakh. Both the Revenue and the assessee appealed against the CIT(A)’s decision.

Issue Involved:

The core issue was whether the amendment made by the Finance Act, 2020—raising the permissible variation between transaction value and stamp duty value from 5% to 10% under Section 56(2)(x)(b)(B)—applies retrospectively to AY 2018–19. The related question was whether the assessee was entitled to relief for the differential value being within the newly increased 10% margin

Tribunal’s Decision:

The ITAT Mumbai held that the amendment introduced by the Finance Act, 2020 is retrospective in nature and thus applicable to the Assessment Year 2018–19. It found that, based on the DVO’s report and the data provided by the assessee, the difference between the purchase value and the stamp duty value exceeded 10% only in respect of one unit (Unit 103), while the other two were within the threshold. The Tribunal remanded the matter to the AO to apply the 10% tolerance as per the amended Section 56(2)(x)(b)(B), and to restrict the addition only to the excess amount beyond that margin. The appeal of the assessee was allowed, and the appeal of the Revenue was dismissed.

5. LTCG on sale of shares and claimed same as exempt under section 10(38)- Manish Devendrakumar Shah vs. Income-tax Officer [2025] 172 taxmann.com 466 (Ahmedabad – Trib.)[25-02-2025]

Facts of the Case:

The assessee, Manish Devendrakumar Shah, filed his return of income for AY 2014–15, claiming exemption under Section 10(38) for Long-Term Capital Gains (LTCG) earned on the sale of shares of Looks Health Services Ltd. (LHSL). Based on information from the Investigation Wing, the Assessing Officer (AO) reopened the assessment under Section 147 and treated the sale of LHSL shares as a bogus transaction. Consequently, the AO denied the exemption and made an addition of ₹1.07 crore under Section 68, alleging the transaction to be an accommodation entry in a penny stock scheme. The AO relied solely on abnormal price fluctuations and the classification of LHSL as a penny stock, without conducting any independent inquiry or providing the assessee access to the investigation report. The Commissioner (Appeals) upheld the AO’s view, branding the transaction as a make-believe arrangement for laundering unaccounted money.

Issue Involved

The key issue was whether the addition under Section 68, treating LTCG from penny stocks as bogus, could be sustained when the assessee had acquired shares through preferential allotment, provided complete documentary evidence, and all transactions were carried out via banking channels without any cash involvement. Also at issue was whether the revenue could rely on third-party reports without furnishing direct evidence or granting cross-examination.

Tribunal’s Decision:

The ITAT Ahmedabad ruled in favour of the assessee, deleting the entire addition under Section 68. The Tribunal held that the assessee had furnished substantial documentary evidence—including demat statements, bank records, share allotment letters, and sale invoices—establishing the genuineness of the transaction. It noted that the shares were acquired directly from the company through preferential allotment with a mandatory lock-in period, which ruled out initial price manipulation. The Tribunal criticised the revenue for failing to bring on record any direct evidence linking the assesse to artificial price rigging or accommodation entries, and for relying solely on assumptions and general market trends. It held that merely labelling a stock as a “penny stock” or observing high price fluctuations is insufficient to invoke Section 68 unless supported by specific material evidence. As such, the entire addition of ₹1.07 crore was deleted, and the appeal of the assesse was allowed in full.

6. Application under section 197 for nil withholding allowed as payments by Indian reseller not shown to be taxable in India at this stage. SFDC Ireland Ltd. Commissioner of Income-tax [2025] 171 taxmann.com 731 (Delhi)[17-02-2025]

Facts of the Case:

SFDC Ireland Ltd., a tax resident of Ireland, entered into a non-exclusive reseller agreement with its Indian affiliate, SFDC India, to sell standardized Customer Relationship Management (CRM) products in India. The company filed an application under Section 197 of the Income-tax Act, 1961, seeking a nil withholding tax certificate on payments received from SFDC India, arguing that its income was not taxable in India as it had no permanent establishment (PE) in India. The Assessing Officer (AO) rejected the application, contending that SFDC India’s role in price determination and contract execution indicated dependency, suggesting a potential PE.

Issue Involved:

The key issue was whether the payments made by SFDC India to SFDC Ireland were chargeable to tax in India, requiring tax deduction at source (TDS), and whether SFDC India constituted a dependent agent PE of SFDC Ireland under the India-Ireland Double Taxation Avoidance Agreement (DTAA).

Tribunal’s Decision :

The Delhi High Court set aside the AO’s order, ruling that there was no prima facie evidence to establish SFDC India as a dependent agent PE. The court emphasized that the reseller agreement clearly defined the relationship as principal-to-principal, with no authority for SFDC India to bind SFDC Ireland. The court directed the AO to issue a nil withholding tax certificate, noting that the income was not taxable in India at this stage. However, it clarified that the ruling would not preclude the AO from examining the taxability in subsequent assessments. The decision was in favor of SFDC Ireland.

7. No Addition of Capital Gains on Jointly Held Property as Assessee is not a Beneficial Owner| Vinod Nihalchand Jain,Mumbai vs Ito Ward 41(3)(4), Mumbai

Facts of the Case:

The assessee, an individual, did not file a return of income for Assessment Year (AY) 2015–16, claiming income was below the basic exemption limit. Based on third-party information that the assessee had sold an immovable property for ₹54 lakhs during the relevant year, reassessment proceedings were initiated under section 147 of the Income Tax Act, 1961. The property was registered in joint names of the assessee, his father, and his brother. The sale deed was executed jointly by the assessee and his brother. The Assessing Officer (AO) treated 50% of the sale consideration (₹27 lakhs) as Long-Term Capital Gains (LTCG) taxable in the hands of the assessee. The CIT(A) upheld the AO’s order with a direction to allow deduction for cost of acquisition if substantiated.

Issue Involved:

Whether the addition of ₹27,00,154/- as LTCG in the hands of the assessee under section 45 of the Act was justified, considering that the assessee claimed he was not the beneficial owner of the property and the entire consideration was paid and received by his brother.

Tribunal’s Decision:

The Tribunal held that the assessee’s brother was the sole beneficial owner of the property, having paid the full purchase consideration and received the entire sale consideration. The assessee’s name was included in the property documents only out of natural love and affection, and no real ownership or beneficial interest was established. Since the brother declared the full sale consideration in his return and claimed exemption under section 54F, and no adverse finding existed in his case, the Tribunal found no justification for taxing the assessee. Consequently, the addition of ₹27,00,154/- as LTCG in the hands of the assessee was deleted and the appeal was allowed.

8. No Addition under Section 69 Based Solely on Survey Statement Without Corroborative Evidence| Assessee vs NFAC, Delhi [ITA No. —/Mum/2025, AY 2014-15, Order dated 21.02.2025]

Facts of the Case:

The assessee, an individual, purchased a flat for ₹1,27,30,000 from M/s Shah Housecon Pvt. Ltd. through a registered agreement dated 15.02.2014. A survey was conducted at the builder’s premises, during which a statement was recorded from its Senior Accountant, Shri Binesh Balakrishnan, alleging on-money payments by buyers. Based on this, the Assessing Officer (AO) added ₹33,00,000 to the assessee’s income as unexplained investment under Section 69 of the Income Tax Act, 1961, despite the assessee filing an affidavit, submitting bank statements, and denying any cash payments. The AO did not permit cross-examination of the person whose statement was relied upon. The CIT(A) upheld the addition.

Issue Involved:

Whether the addition of ₹33,00,000 under section 69 as unexplained investment was sustainable solely based on a third-party statement recorded during a survey, without granting cross-examination or bringing corroborative evidence on record.

Tribunal’s Decision:

The Tribunal held that the addition under Section 69 was not justified. It observed that:

- The AO relied solely on a survey statement under Section 133A, which has no evidentiary value unless supported by independent material.

- The assessee denied making any cash payment and submitted an affidavit and bank proof of payments.

- The assessee requested cross-examination, which was denied.

- No independent enquiry was conducted by the AO, and no corroborative evidence was brought on record.

- The coordinate bench decision in M/s Yash Synthetic Pvt. Ltd. was followed, which involved the same builder and similar facts.

Accordingly, the addition was deleted, and the appeal was allowed.

9. No Addition for Alleged Cash Transaction without Evidence or Opportunity to Cross-Examine | Enrich Hair and Skin Solutions Pvt. Ltd. vs ACIT, Range 14(1)-2, Mumbai

Facts of the Case:

The assessee, Enrich Hair and Skin Solutions Pvt. Ltd., engaged in beauty salon services, filed its return for AY 2007-08 declaring income of ₹1,20,73,770. The return was reopened under section 147 based on information from the Investigation Wing alleging that the assessee paid ₹47,00,000 in cash to M/s. Lake View Developers (Hiranandani Group) for purchasing a shop at Ventura Building. The assessee denied any such transaction, stating that the only dealing with Lake View Developers was in AY 2009-10 for renting a property, for which a security deposit of ₹4,14,000 was paid and subsequently refunded. The AO made an addition under section 69 for ₹47,00,000 as unexplained investment based on third-party statements without sharing any such material with the assessee or granting an opportunity for cross-examination.

Issue Involved:

Whether the addition of ₹47,00,000 as unexplained investment under section 69 was sustainable when based solely on third-party information and without any corroborative evidence, especially when the assessee was not granted an opportunity to rebut or cross-examine the sources relied upon.

Tribunal’s Decision:

The Tribunal noted that no documentary evidence or statement justifying the addition was provided by the AO, nor were the assessee’s explanations refuted with evidence. It observed that mere assumptions based on the general practice of cash dealings and the assessee’s past tenancy at a Hiranandani property did not justify the addition. Since the only confirmed transaction was a rental security deposit of ₹4,14,000 refunded in the same year, and no material evidence of cash payment in AY 2007-08 was on record, the Tribunal held the addition under section 69 to be unjustified and deleted it. The appeal was allowed.